The World That Built Them Is Gone: The World Bank, the IMF, and the Crisis of Technocratic Legitimacy

Author's Note: My interest in the legitimacy of international institutions emerged through graduate work in global healthcare leadership at the University of Oxford, participation in a board director program led by Professor Andrew Kakabadse at Henley Business School, and subsequent research into governance, development, and institutional authority. While debates surrounding the IMF and World Bank are often framed in terms of representation and reform, I became increasingly interested in a different question: how institutions sustain legitimacy when the assumptions that once justified their authority are no longer universally accepted.

The International Monetary Fund (IMF) and the World Bank were created in the aftermath of World War II, following the Bretton Woods Conference, to help stabilize the global economy and support economic development. Over time, they became two of the most influential institutions in the international system. The IMF provides emergency financing and policy guidance to countries facing financial crises, while the World Bank finances development projects and advises governments on economic policy. Both help shape how countries think about growth, debt, investment, poverty reduction, and economic reform.

Today, however, these institutions face growing criticism from both emerging powers and developing economies. While their concerns differ, both groups question whether governance structures created in the aftermath of the Second World War remain fit for a dramatically changed global economy. Countries across Africa, Asia, Latin America, and parts of the Middle East argue that the governance arrangements of the IMF and World Bank no longer reflect contemporary economic realities. Meanwhile, countries such as China, India, Brazil, Indonesia, and others now occupy positions of economic influence far greater than those they held when the institutions were originally designed.

Whether these criticisms are ultimately justified is a separate question. What matters for the purposes of institutional analysis is that they exist, that they are becoming more widespread, and that they challenge assumptions that were once taken for granted. As a result, debates over quota reform, voting shares, board representation, leadership selection, and institutional authority have become more prominent within discussions of global governance.

The significance of this trend extends well beyond the specific reforms being proposed. The issue is not simply that some states seek greater influence within existing institutions. Nor is it solely a question of whether voting shares should better reflect contemporary economic realities. What is being challenged is not merely the distribution of authority, but the legitimacy of the ideas that have long justified it. Assumptions about development, governance, and economic management that once commanded broad acceptance now face sustained scrutiny.

At first glance, the dispute appears to be about representation. If the distribution of global economic power has changed, many argue, then the distribution of authority within global institutions should change as well. Yet this framing captures only the visible layer of the conflict. The more important question is who possesses the authority to help establish the categories through which economic performance is evaluated.

The argument no longer concerns only who governs these institutions. It concerns the frameworks through which they govern. Disputes over debt sustainability models, development indicators, governance rankings, risk assessments, and policy conditionality have exposed a conflict over whose knowledge counts, whose assumptions prevail, and whether the institutions' understanding of development retains the universal legitimacy it once claimed.

The issue is no longer simply whether developing countries possess sufficient influence within existing institutions. It is whether the institutions themselves continue to command the authority they once enjoyed as interpreters of economic reality through mechanisms such as the IMF's country-level oversight or bilateral surveillance, and the World Economic Outlook.

For much of the postwar era, the IMF and World Bank derived legitimacy not merely from their resources or formal mandates, but from a broader belief that they possessed the expertise necessary to guide economic development through publications such as the World Development Report, manage financial instability, and identify sound policy. Their authority rested on the assumption that they understood the system they were helping to govern through mechanisms such as IMF surveillance and economic assessment.

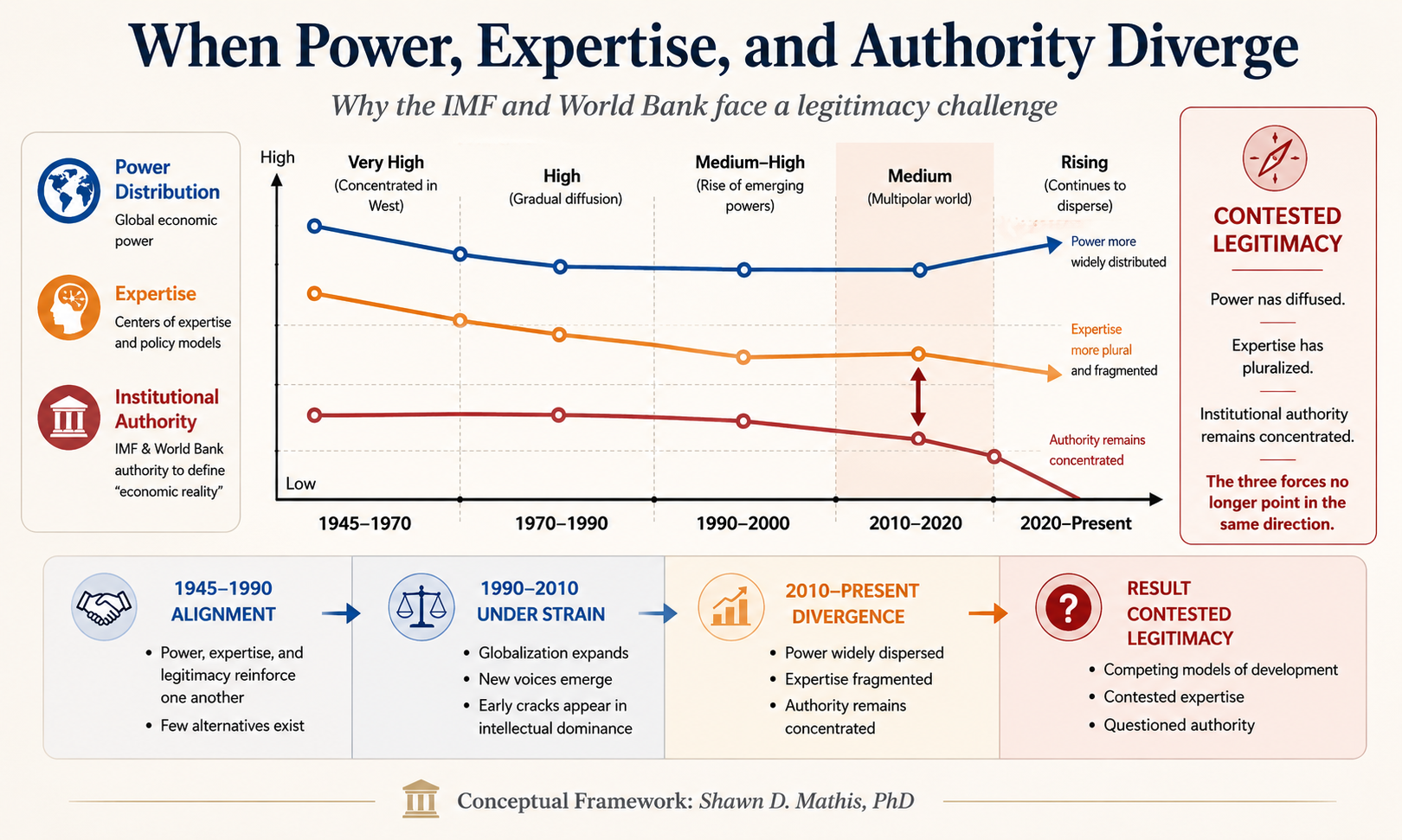

Today, that assumption is being questioned. The institutions were built when power, expertise, and legitimacy were mutually reinforcing. Their legitimacy crisis emerges because those forces are no longer aligned. Power has become more widely distributed, knowledge has become more plural, but authority remains concentrated within institutions whose claims to expertise are contested.

The contemporary debate, thus, extends far beyond voting shares, board seats, or governance reform. At stake is a more fundamental question: who possesses the authority to establish the standards by which sound economic policy, responsible governance, acceptable risk, and successful development are judged? As competing development experiences, alternative policy models, and new centers of expertise emerge—as reflected in institutions and research programs such as the UNCTAD Trade and Development Report—the IMF and World Bank find themselves confronting challenges to their power and to the intellectual foundations upon which their authority has long rested.

The central question facing the IMF and World Bank is therefore not whether they can adapt their governance structures to reflect a changing distribution of power. It is whether institutions that once derived authority from claims of superior expertise can retain that authority once those claims themselves become contested. That question now sits at the center of the debate over global economic governance.

The crisis confronting the IMF and World Bank is not that global power has shifted. It is that power, expertise, and legitimacy no longer point in the same direction.

The IMF and World Bank emerged from the ruins of the Second World War at a singular moment in modern history. Economic power, financial capital, institutional capacity, and technical expertise appeared concentrated in the same places. The United States possessed unparalleled economic strength, Western Europe remained the center of much of the world's financial architecture, and the institutions created at Bretton Woods reflected that distribution of power.

Their authority, however, rested on more than power alone. The postwar order was sustained by a powerful assumption: those who possessed the greatest economic influence also possessed the knowledge necessary to govern an interconnected world economy. Authority was accepted not simply because it existed, but because it appeared justified by expertise.

The IMF and World Bank were never designed to be democratic institutions. They were designed to be functional institutions. Their legitimacy derived less from equal representation than from the belief that they could deliver stability, coordinate international economic relations, support development, and reduce the economic fragmentation that had helped destabilize the interwar world. In this sense, the Bretton Woods system transformed material power into institutional authority through claims of technical competence.

For much of the postwar era, that arrangement appeared successful. International trade expanded, capital flows deepened, and economic development accelerated across much of the world. Financial crises, while hardly absent, appeared manageable within an international framework shaped in substantial part by the institutions themselves. Their recommendations carried weight not merely because they controlled resources, but because they were widely regarded as authoritative interpreters of economic reality.

The durability of the postwar order depended upon that alignment. Countries routinely disagreed with particular policies, lending decisions, or reform programs, but comparatively few challenged the institutions' underlying authority to define what constituted sound economic management, responsible governance, or successful development. Disagreements focused on policy. They rarely extended to legitimacy.

The world in which that arrangement emerged no longer exists. Economic activity has become more geographically distributed. New centers of capital, production, innovation, and finance have emerged. Different development experiences have produced competing interpretations of economic success, while expertise itself has become more pluralistic, decentralized, and difficult for any single institution to monopolize. What has changed is not merely the distribution of power. Competing centers of expertise have emerged as well. The central question is no longer whether the IMF and World Bank possess formal authority, but whether authority derived from expertise remains persuasive once expertise itself becomes contested. Institutions can survive disagreement over policy. They struggle to maintain legitimacy when disagreement extends to the assumptions through which policy is understood. The original bargain rested on a simple premise: those who possessed the greatest power also possessed the greatest understanding of how the system worked. The contemporary crisis emerges because that premise no longer commands automatic assent.

The most visible challenge confronting the IMF and World Bank is also the easiest to understand. The institutions were designed for a world in which economic power, financial capital, and institutional influence were concentrated among a relatively small group of Western states. The governance structures established at Bretton Woods reflected that reality. Voting power, leadership arrangements, and decision-making authority were built upon assumptions about where power resided and who would shape the future of the international economy.

For a time, those assumptions broadly reflected the world as it existed. Over the past half-century, however, economic activity has become far more geographically distributed. New centers of production, finance, innovation, and consumption have emerged across Asia, Latin America, the Middle East, and parts of Africa. Countries that once occupied the periphery of the global economy now play central roles in global growth, trade, investment, and capital formation. While the distribution of economic power changed dramatically, the architecture of institutional authority changed far less.

This divergence created the first legitimacy gap. Institutions derive authority not merely from legal mandates but from their ability to reflect the realities they claim to govern. When the relationship between power and representation diverges too far, authority begins to appear inherited rather than earned. Governance structures resemble historical artifacts rather than contemporary settlements.

Calls for quota reform, voting reform, leadership reform, and greater representation are manifestations of this tension. They are attempts to reconcile a changing distribution of power with institutions designed for an earlier era. Viewed in isolation, this appears to be the central problem. Yet history is filled with shifting distributions of power. Great powers rise and decline, economic centers move, and institutions adapt—sometimes successfully and sometimes not. There is nothing historically unusual about demands for greater representation following changes in relative power.

What makes the present moment distinctive is that the redistribution of power has exposed a second and more consequential challenge. The states seeking greater influence are not merely demanding a larger role within the existing framework. They are also questioning assumptions embedded within the framework itself. The dispute extends beyond representation and into the production of governance knowledge itself. It concerns whose experiences count as evidence, which development paths are treated as models, and who possesses the authority to make those judgments.

Seats can be redistributed, voting formulas can be revised, and leadership arrangements can be renegotiated. Questions of authority are more difficult because they concern the intellectual foundations of governance rather than its formal structures. Voting reform can redistribute power. It cannot resolve disagreements over how risk is measured, how development is defined, how policy success is evaluated, or how economic reality itself is interpreted.

The distinction is consequential. Representation determines who participates in decision-making. Authority determines whose interpretation prevails. The first legitimacy gap emerged because economic power shifted while governance structures remained largely intact. The second emerged because economic power shifted while the intellectual architecture through which governance is exercised remained substantially unchanged.

The contemporary debate surrounding the IMF and World Bank is often presented as a dispute about representation. In reality, representation is only the visible layer of the conflict. Beneath disagreements over voting shares, quotas, and governance reform lies a deeper question: what happens when the foundations upon which institutional authority rests become contested?

The IMF and World Bank do far more than lend money, advise governments, or provide technical assistance. They help define the categories through which the global economy is understood.

Every year, governments, investors, central banks, development agencies, and financial markets rely upon assessments produced by these institutions. Their reports influence how countries are evaluated, how risks are priced, how investment decisions are made, and how policy choices are judged. The institutions do not merely participate in the global economy; they help shape the framework through which it is interpreted.

That authority did not emerge simply because the institutions possessed expertise. Many organizations possess expertise. The authority of the IMF and World Bank emerged because their expertise was embedded within a postwar order in which power, institutional influence, and technical knowledge appeared aligned. Their judgments carried unusual weight because the institutions themselves occupied a privileged position within the international economic system.

For decades, that arrangement appeared natural. When the IMF described a country as fiscally vulnerable, markets paid attention. When the World Bank evaluated institutional quality, investors took notice. When either institution concluded that a policy was sustainable, credible, or reform-oriented, those judgments influenced everything from borrowing costs to development financing.

Such assessments are usually presented as technical exercises. They appear to be measurements. Yet before any model can measure reality, someone must decide which variables matter, which outcomes count as success, which risks deserve attention, and which tradeoffs are considered acceptable. What appears to be neutral description frequently rests upon prior assumptions about markets, states, development, stability, and economic performance.

This is not a failure. It is a characteristic of institutional governance. Debt sustainability frameworks, governance indicators, poverty measurements, investment climate rankings, and conditionality models do not emerge from nature. They are constructed systems of interpretation that reflect choices about what should be measured and how those measurements should be understood.

For much of the postwar period, those choices attracted relatively little scrutiny because the authority of the institutions themselves was rarely questioned. The contemporary dispute is therefore not primarily about whether particular assessments are correct. Governments have always disagreed with policy recommendations. The dispute concerns the authority of the frameworks through which those assessments are made.

Countries challenge assumptions embedded within debt sustainability models, governance rankings, fiscal targets, development indicators, and policy conditionality. The argument no longer centers exclusively on conclusions. It concerns the standards from which those conclusions are derived. The legitimacy question is no longer whether institutions possess expertise, but whether they possess the authority to determine the terms through which expertise is exercised.

The deepest source of tension is not that developing countries possess too few votes within the institutions. It is that the institutions possess unusual authority to describe them. They classify countries as stable or unstable, credible or uncredible, reforming or resistant, attractive or unattractive to investment. Those classifications do not merely record reality. They influence it.

A country classified as risky may face higher borrowing costs. A government deemed fiscally irresponsible may encounter pressure to alter domestic policy. A development strategy judged inconsistent with accepted orthodoxy may struggle to attract external support regardless of its domestic political legitimacy. In this sense, expertise becomes a form of governance. The power to define acceptable risk, sound policy, fiscal responsibility, institutional quality, or successful development is itself a form of authority because it shapes the range of choices that appear rational and narrows the range of choices that appear possible.

This is the second legitimacy gap. Authority to interpret economic reality remains concentrated within institutions whose expertise is no longer accepted as self-validating. Once the authority to interpret reality becomes contested, legitimacy can no longer be secured through representation alone. The institutions are confronting a world in which authority depends not simply upon what they know, but upon whether others continue to accept their right to define what counts as knowledge in the first place.

Modern governance operates through numbers. Governments are ranked, economies are scored, debt is modeled, poverty is quantified, institutional quality is assessed, and risk is calculated. What appears to be a world of political judgment commonly presents itself as a world of technical evaluation.

The reliance on metrics reflects a practical necessity. Modern institutions govern at a scale that exceeds direct observation. No investor can study every economy in detail, no development agency can fully account for every local condition, and no international institution can evaluate every political and social circumstance individually. Metrics reduce complexity to manageable categories and create a common language through which decisions can be made. Their importance lies not only in their ability to simplify information, but also in their ability to shape decisions.

A country's borrowing costs may be influenced by assessments of fiscal sustainability. Investment flows may be affected by evaluations of governance quality. Access to financing may depend upon judgments about debt vulnerability, institutional capacity, or policy credibility. In practice, these measurements do not merely describe economic reality. They help organize it.

The more consequential question concerns the measurement systems themselves. Every metric begins with a prior judgment about what should be measured. Before debt can be modeled, someone must decide what constitutes risk. Before governance can be assessed, someone must decide what constitutes good governance. Before poverty can be quantified, someone must decide which dimensions of human well-being matter and which do not. Measurement follows judgment; it does not replace it.

Consider the seemingly straightforward concept of fiscal responsibility. The term routinely appears self-evident, yet every attempt to measure fiscal responsibility requires choices. Should governments prioritize debt reduction or productive investment? Should borrowing for infrastructure be evaluated differently from borrowing for consumption? Should future growth be weighed against present fiscal restraint? How should unemployment, social stability, industrial capacity, or climate vulnerability be incorporated into assessments of sustainability? No statistical model can answer these questions on its own because they ultimately require judgments about priorities.

The same pattern appears throughout the architecture of global economic governance. Debt sustainability frameworks contain assumptions about acceptable risk. Governance indicators contain assumptions about institutional quality. Investment climate rankings contain assumptions about what makes an economy attractive to capital. Poverty measures contain assumptions about what constitutes human welfare. The metrics may be technical, but the assumptions embedded within them are not.

This observation should not be mistaken for a critique of measurement itself. Modern economies cannot function without analytical tools capable of reducing complexity. The issue is not whether metrics are necessary. The issue is whether they are neutral. Every measurement system illuminates certain realities while obscuring others. What is measured becomes visible; what is not measured in practice becomes politically invisible.

A debt model may capture repayment capacity while overlooking social fragility. A fiscal framework may emphasize budget discipline while assigning less weight to long-term developmental capacity. An investment ranking may reward openness to capital while paying little attention to industrial resilience, economic sovereignty, or strategic vulnerability. Over time, these choices accumulate. What begins as measurement gradually becomes governance.

The significance of this shift extends beyond methodology. Concepts that for much of the postwar era were treated as objective economic facts may function as vehicles for particular policy priorities. Social spending can appear primarily as a fiscal cost. Creditor confidence can become synonymous with stability. Austerity can be framed as discipline. Industrial policy can be treated as distortion. Capital mobility can appear natural rather than political. Debt repayment can become an unquestioned obligation rather than one consideration among many. None of these conclusions emerge automatically from data. They emerge from frameworks that determine how data is interpreted.

This is why disputes over metrics have become disputes over legitimacy. The challenge confronting the IMF and World Bank is not simply that countries disagree with particular policies. It is that they question the categories through which those policies are justified. The dispute is no longer only about outcomes. It is about the standards used to produce them.

Once the legitimacy of those standards becomes contested, expertise becomes more difficult to separate from governance. What once appeared to be neutral analysis begins to appear, at least to some of those being governed, as a particular vision of economic order expressed through numbers. Metrics are never merely measurements. They are instruments through which power becomes visible, comparable, and ultimately governable.

Every society faces constraints. Debt must be serviced, inflation must be contained, investment must be attracted, jobs must be created, infrastructure must be built, and social stability must be maintained. Governments do not choose whether constraints exist. They choose which constraints take priority. That distinction sits at the center of the contemporary debate surrounding the IMF and World Bank.

Different actors experience those constraints differently. A finance ministry may focus on debt sustainability, citizens on employment, international lenders on fiscal deficits, households on food prices, and investors on policy predictability. Governments themselves may prioritize industrial development, political stability, or long-term economic transformation. All are responding to real constraints. The question is which constraints acquire priority within systems of governance.

For much of the postwar era, international economic governance has tended to treat certain constraints as especially urgent. Debt ratios, inflation targets, fiscal deficits, foreign reserves, and market confidence are within these frameworks treated as realities requiring immediate adjustment. Other constraints—unemployment, poverty, industrial weakness, social fragmentation, demographic pressures, or climate vulnerability—are frequently acknowledged but rarely granted the same status.

This hierarchy is not simply technical. It reflects a judgment about necessity. Every system of governance must decide which problems are treated as binding constraints and which are treated as consequences, tradeoffs, or secondary concerns. Those decisions shape policy long before any particular policy is adopted. The contemporary dispute has emerged because many governments no longer regard this hierarchy as self-evident. The disagreement is not simply about debt, inflation, deficits, or development strategy. It concerns who possesses the authority to determine which constraints are regarded as unavoidable in the first place. The question reaches beyond economics because different definitions of necessity produce different forms of governance. A society that treats debt repayment as an overriding necessity will govern differently from a society that treats employment as an overriding necessity. A government that prioritizes investor confidence above all else will make different choices from one that prioritizes industrial capacity, social cohesion, or political stability. None of these priorities emerge automatically from economic data. They reflect judgments about what must be protected, what may be sacrificed, and what constitutes acceptable risk.

This is why the legitimacy crisis confronting the IMF and World Bank cannot be reduced to a dispute over policy. The dispute concerns the authority to determine necessity itself. The power to determine which constraints matter most, and which sacrifices become acceptable in response to them, is among the most consequential forms of authority any institution can possess.

Stability is among the most frequently invoked objectives in international economic governance. Governments seek it, investors seek it, and international institutions are frequently judged by their ability to preserve it. Yet stability is not a self-explanatory concept. A country can maintain stable debt repayment while unemployment rises, preserve exchange-rate stability while public services deteriorate, or restore investor confidence while political unrest intensifies. What appears stable from one vantage point may appear deeply unstable from another.

This distinction is not merely semantic. It reflects a fundamental question about governance. Every definition of stability privileges certain risks over others and certain constituencies over others. For creditors, stability means confidence that debts will be repaid and macroeconomic conditions will remain predictable. For governments confronting poverty, unemployment, weak industrial capacity, or social fragmentation, stability may mean something entirely different: social cohesion, political legitimacy, food security, or the capacity to create jobs. Neither perspective is inherently irrational. The question is which perspective acquires the status of necessity.

For much of the postwar era, international economic governance has tended to treat financial stability as the foundation upon which all other forms of stability depend. Debt sustainability, price stability, fiscal discipline, reserve adequacy, and investor confidence occupy a privileged position within policy frameworks because they are regarded as prerequisites for everything else. That hierarchy appeared broadly self-evident for much of the period in which the Bretton Woods institutions exercised their greatest authority. Today, that assumption commands less automatic acceptance. The contemporary dispute is not whether financial stability matters. It is whether financial stability should automatically take precedence over other forms of stability. Why is social instability considered an acceptable price for achieving financial stability, while financial instability is rarely considered an acceptable price for preserving social stability?

The question exposes a distinction that discussions of stability in practice conceal. The issue is not whether stability should be pursued, but which form of stability is treated as reality and which forms are treated as preferences. Once that distinction becomes visible, stability ceases to function as a neutral objective and begins to appear as a political category reflecting particular judgments about risk, priority, and acceptable sacrifice. At that point, the debate can no longer be confined to technical questions of economic management. It becomes a debate about authority. Who possesses the authority to decide which risks matter most, which forms of instability deserve immediate attention, and which sacrifices are acceptable in pursuit of stability itself? That question now sits near the center of the legitimacy crisis confronting the IMF and World Bank.

The consequences of competing definitions of necessity and stability become most visible during periods of fiscal crisis. When countries confront mounting debt burdens, international assistance is frequently accompanied by demands for adjustment. Governments are encouraged—or required—to reduce spending, reform subsidies, limit public-sector wages, raise taxes, or restructure social programs. Such measures are usually presented as responses to economic necessity. In many cases, they may be. Defenders of fiscal adjustment argue that prioritizing financial stability protects broader social objectives over the long term by preventing more severe economic dislocation.

Necessity alone, however, does not determine how adjustment is distributed. Every fiscal crisis creates the same underlying problem: there are not enough resources to satisfy every claim simultaneously. Creditors expect repayment, citizens expect public services, workers expect wages, businesses seek stability, governments seek political legitimacy, and future generations inherit the consequences of present decisions. Adjustment, then, requires choices. Economics can illuminate those choices, but it cannot eliminate them.

This is why austerity is never merely a fiscal program. It is also a mechanism for ranking competing claims on limited resources. Decisions must be made about whose interests will be protected, whose sacrifices will be considered necessary, and whose losses will be treated as unavoidable. Those decisions cannot be derived from spreadsheets alone. They require judgments about obligation, legitimacy, fairness, and political priority.

The significance of austerity extends beyond spending cuts or budget targets. The central issue is not simply that resources are reduced. It is that some claims acquire privileged status while others must continually justify themselves. Debt repayment is in practice treated as a binding obligation, while social programs are treated as adjustable expenditures. Creditor confidence is frequently regarded as a necessity, while social protection is treated as a tradeoff. Whether one agrees with those priorities or not, they reflect a hierarchy of claims rather than a neutral economic fact.

This is the source of much of the controversy surrounding austerity. Critics, at times, are less concerned with the existence of adjustment than with the way adjustment is justified. What appears to be a technical discussion about fiscal discipline frequently contains implicit judgments about which obligations matter most and which objectives deserve priority. The dispute is not only about economics. It is also about authority.

Once that hierarchy becomes visible, debates over austerity become difficult to contain within the language of technical policy. The question is no longer whether sacrifices are necessary, but who possesses the authority to determine which sacrifices are necessary and whose interests will bear the costs. At that point, the debate moves beyond fiscal policy and becomes a debate about legitimacy itself.

The legitimacy crisis confronting the IMF and World Bank is discussed in terms of power, representation, expertise, or governance. Yet beneath these debates lies a less visible question: who possesses the authority to make choices without first having to justify their right to make them?

In theory, sovereignty implies equality. States possess different levels of power, but each retains the formal right to determine its own political and economic priorities. In practice, however, sovereignty has never been exercised equally. Some states are granted broad discretion to pursue unconventional policies, absorb mistakes, and experiment with alternative approaches. Others are expected to explain, defend, and justify their decisions before they are regarded as legitimate.

This distinction matters because authority rests as much on expectations as it does on rules. The most powerful actors within any system commonly possess the privilege of acting without explanation. Weaker actors frequently carry the burden of proving that their choices are reasonable, responsible, or consistent with accepted standards.

For much of the postwar era, this arrangement appeared natural. The institutions of global economic governance emerged from a world in which expertise, capital, and authority were concentrated in a relatively small number of advanced economies. Policy advice largely flowed in one direction. Some countries defined the lessons. Others were expected to learn them. The distinction was rarely stated explicitly. It was embedded within the structure of development itself.

Countries receiving assistance were expected to reform. Countries providing assistance were assumed to possess the knowledge necessary to determine what reform required. Borrowers were evaluated. Creditors performed the evaluation. Developing countries were encouraged to adopt institutional arrangements, policy frameworks, and governance practices that had emerged elsewhere. The authority to judge success remained concentrated among those already occupying positions of influence within the international system. This is one of the least discussed legacies of the postwar order.

The most enduring consequence of hierarchy is not unequal power. It is unequal authority. Over time, many countries accepted this arrangement because the broader system appeared to deliver results. Economic growth expanded. Poverty declined across large portions of the world. International integration appeared to offer a credible path toward prosperity. The distinction between teacher and student appeared less contentious because the underlying promise still retained credibility. That condition has weakened.

The rise of new economic powers, alternative development experiences, and competing sources of expertise has complicated the assumption that successful development follows a single path. Countries that have achieved growth through different institutional arrangements question why particular policy frameworks continue to enjoy privileged status within international institutions. Experiences once treated as exceptions now challenge models that were, for much of the postwar era, presented as universal.

As a result, the contemporary dispute extends beyond representation or voting shares. It concerns the authority to establish what constitutes successful development in the first place. The issue is not whether countries should learn from one another. It is who possesses the authority to determine which lessons matter, which experiences count as evidence, and which development paths are regarded as legitimate. The legitimacy crisis confronting the IMF and World Bank reflects a growing challenge to a hierarchy of authority that long appeared natural. The question is no longer simply who governs; rather, it is who possesses the standing to determine what good governance means. That distinction helps explain why reform has become so difficult. Voting shares can be adjusted, board representation expanded, and leadership arrangements renegotiated. The authority to define the standards through which others are evaluated is far more difficult to share. Once that authority becomes contested, institutional legitimacy becomes more difficult to sustain than institutional power itself.

For much of the postwar era, the legitimacy of the international economic order rested on more than institutional authority. It also rested on a promise. The promise was convergence. Countries occupying the periphery of the global economy were told that integration, reform, investment, and development would gradually narrow the gap separating them from the world's most advanced economies. Different institutions emphasized different policies, but the underlying narrative remained remarkably consistent. Economic modernization would produce rising prosperity. The distance between rich and poor countries would steadily diminish. The future would become more equal than the past. That promise mattered because legitimacy depends not only upon authority, but upon confidence that authority is leading somewhere worth going. Countries within these frameworks accept unequal arrangements when they believe those arrangements lead toward a more desirable future. Hierarchies become easier to tolerate when they appear temporary. Authority becomes easier to accept when it appears productive.

For much of the postwar period, the promise retained considerable credibility. Hundreds of millions of people were lifted from poverty. International trade expanded. Living standards improved across large portions of the developing world. Economic integration appeared to validate the broader logic of the system.

Yet convergence proved far less uniform than many expected. Some countries advanced rapidly. Others stagnated. Some integrated successfully into global markets. Others experienced repeated cycles of debt, adjustment, and vulnerability. Economic growth in practice occurred alongside rising inequality, institutional fragility, or political instability. The result was not a single development story, but multiple competing development experiences.

The authority of the IMF and World Bank was strengthened by the belief that they possessed knowledge capable of helping countries achieve prosperity. When confidence in that proposition weakens, authority becomes more difficult to sustain. Questions that were once directed toward implementation gradually become directed toward the framework itself. Once confidence in convergence weakens, legitimacy becomes harder to derive from expertise alone. Institutions may continue to possess authority, resources, and influence. What becomes more difficult is sustaining confidence that the future they describe is the future others should pursue. The postwar order was built upon the belief that different societies were moving toward a broadly common destination. The contemporary legitimacy crisis emerged as successful development experiences challenged the assumption that there was only one route to get there.

The legitimacy crisis confronting the IMF and World Bank cannot be understood solely through questions of representation, expertise, or development. It is also shaped by a structural reality that receives far less attention: the institutions are frequently called upon to manage vulnerabilities that emerge from the same international economic order they were created to support.

The postwar system was designed to promote economic growth through expanding trade, investment, financial integration, and cross-border flows of capital. By many measures, it succeeded. International commerce expanded dramatically, global production became interconnected, and hundreds of millions of people were incorporated into a more integrated world economy. The gains generated by this process were substantial and, in many respects, historically unprecedented.

Yet integration produced vulnerabilities alongside prosperity. The same financial openness that facilitates investment can accelerate capital flight. The same access to international credit that supports development can contribute to debt accumulation. The same global markets that create opportunities for growth can transmit financial shocks across borders with remarkable speed. As economies become more interconnected, they in practice become more exposed to disturbances originating beyond their own borders.

This outcome should not be viewed as a failure of globalization. The forces that increase efficiency, connectivity, and opportunity frequently increase vulnerability as well. Economic integration does not eliminate risk; it redistributes and transforms it.

The IMF and World Bank therefore occupy an unusual position within the international order. They are expected to stabilize the consequences of disruptions that emerge within a system whose broader architecture they were created to sustain. Financial crises, debt crises, balance-of-payments crises, and development crises are commonly treated as discrete events requiring technical intervention. Yet many of these episodes arise from structural features of an interconnected global economy rather than from isolated policy mistakes.

The IMF and World Bank have repeatedly demonstrated their capacity to provide emergency financing, coordinate policy responses, and mitigate economic instability. Yet the persistence of recurring crises inevitably raises broader questions about the relationship between crisis management and system design. Critics disagree about the source of recurring vulnerability. Some argue that international institutions fail to address underlying structural conditions, while others contend that such vulnerabilities are an unavoidable feature of a highly interconnected global economy.

The precise diagnosis matters less than the broader implication. Repeated intervention can gradually alter how institutional authority is perceived. An institution initially derives legitimacy from its ability to solve problems. Over time, however, observers begin to distinguish between solving problems and managing their recurrence. The more frequently institutions are called upon to address similar crises, the more likely questions arise about whether the underlying sources of vulnerability remain unresolved.

This dynamic has become visible in contemporary debates surrounding global economic governance. The issue is no longer simply whether the IMF and World Bank possess the expertise necessary to respond to crises. It is whether institutions can sustain legitimacy when they are repeatedly tasked with managing vulnerabilities that appear embedded within the operation of the system itself.

The postwar order generated extraordinary gains in prosperity, investment, and economic integration. It also generated new forms of exposure that accompanied those gains. The legitimacy challenge confronting the IMF and World Bank emerges from the fact that they are asked to manage one side of that equation while possessing only limited authority over the other.

The legitimacy challenges confronting the IMF and World Bank are widely recognized. Debates over representation, expertise, governance, conditionality, and institutional authority have persisted for decades. Yet despite repeated calls for reform, meaningful change has proceeded slowly and incrementally.

Part of the answer lies in the nature of institutional authority itself. Institutions are not neutral containers that can be redesigned at will. They embody historical settlements that reflect particular distributions of power, influence, and interests. The governance structures of the IMF and World Bank were not accidental. They emerged from the political realities of the postwar order and continue to reflect many of those realities today.

The actors with the greatest ability to authorize reform are often the actors whose influence is most likely to be affected by reform. Changes in voting shares, leadership selection, governance arrangements, or institutional priorities are rarely technical adjustments. They alter the distribution of authority within the organization itself.

As a result, reform debates frequently become caught between two competing pressures. On one side lies the need for institutions to adapt to changing realities. On the other lies the desire of existing stakeholders to preserve arrangements that continue to provide influence, predictability, or strategic advantage.

The challenge extends beyond formal governance structures. Institutional authority is also embedded within habits of thought, professional networks, analytical frameworks, and accepted forms of expertise. Representation can be adjusted relatively quickly through procedural reform. Altering the intellectual foundations through which authority is exercised is considerably more difficult.

This helps explain why legitimacy disputes commonly persist even when reforms occur. Voting formulas can be revised, board representation expanded, and leadership selection procedures reconsidered. Yet many of the underlying questions raised throughout this debate remain largely unchanged. Who defines development? Who determines acceptable risk? Who decides which constraints are binding and which sacrifices are necessary?

These questions are difficult to resolve because they concern authority rather than procedure. Procedures can be modified through negotiation. Authority depends upon recognition. Institutions remain legitimate not simply because rules grant them power, but because others continue to accept their right to exercise that power.

Governance disputes concern how authority is distributed. Legitimacy disputes concern whether authority remains persuasive. The former can, in practice, be addressed through reform. The latter requires rebuilding confidence in the principles through which authority is exercised. The challenge confronting the IMF and World Bank extends beyond redesign. The issue is whether authority itself can be renewed without abandoning the institutional foundations upon which it was originally built.

That question has no procedural solution. It is ultimately a question about whether power, expertise, and legitimacy can once again be brought into alignment. Until that occurs, debates over reform are likely to remain debates about symptoms rather than resolutions.

By this point, the legitimacy crisis confronting the IMF and World Bank can no longer be understood as a dispute about representation alone. Nor can it be reduced to disagreements over voting shares, governance reform, debt sustainability, fiscal policy, development indicators, or institutional expertise. Each of these debates reflects a larger question that sits beneath them all: what vision of economic order should govern the international system?

For much of the postwar era, that question appeared largely settled. The institutions created at Bretton Woods operated within a framework that treated certain economic objectives as broadly self-evident. Economic growth was assumed to be desirable, financial stability was assumed to be necessary, and market integration was assumed to be beneficial. Development was frequently understood as a process through which poorer societies gradually moved toward institutional and economic arrangements already established within the advanced industrial world. These assumptions were never purely technical. They reflected judgments about what economic life should prioritize, which risks deserved attention, what obligations governments owed their citizens, and what responsibilities societies owed future generations. In doing so, they embodied a particular vision of prosperity, order, and progress.

For decades, those judgments appeared sufficiently persuasive that they attracted relatively little scrutiny. Economic expertise and institutional authority reinforced one another, and the assumptions embedded within policy frameworks for much of the postwar era appeared less as interpretations than as descriptions of reality itself. The contemporary debate has altered that perception. Arguments about debt sustainability frequently contain assumptions about the relative importance of creditors and debtors. Arguments about fiscal discipline within these frameworks contain assumptions about the relationship between present sacrifice and future prosperity. Arguments about governance reform contain assumptions about the nature of effective institutions. Even discussions of economic growth contain implicit judgments about distribution, inequality, industrial development, environmental sustainability, and social welfare.

The issue is not that such assumptions exist. No system of governance can function without them. The issue is that assumptions once treated as universal appear contingent, contestable, and historically specific. This helps explain why many contemporary disputes remain resistant to technical resolution. Technical expertise can estimate debt burdens, model economic outcomes, and evaluate policy tradeoffs. It cannot determine what societies should value most. Questions concerning fairness, obligation, risk, prosperity, and legitimacy inevitably extend beyond economics because they involve competing visions of the good society.

The legitimacy challenge confronting the IMF and World Bank emerges from precisely this tension. The institutions continue to possess substantial expertise, resources, and influence. What has become more difficult is sustaining confidence that the values embedded within their frameworks should continue to function as universal standards for a diverse international system. The debate therefore extends beyond policy and into the realm of authority—not simply the authority to lend, advise, monitor, or evaluate, but the authority to define what constitutes sound economic management, responsible governance, successful development, and acceptable risk.

Beneath disagreements over quotas, voting shares, adjustment programs, governance indicators, and development strategies lies a more fundamental contest over who possesses the standing to establish the principles through which economic life should be organized. The question confronting the IMF and World Bank is therefore not simply whether they can reform their governance structures or adapt their policy frameworks. It is whether institutions whose authority was built upon particular assumptions about economic order can retain legitimacy in a world where those assumptions are no longer universally accepted. That question extends far beyond the future of any individual institution. It is becoming one of the defining questions of global governance itself.

The contemporary debate surrounding the IMF and World Bank is presented as a dispute about representation. Developing countries seek greater influence, emerging powers seek larger voting shares, and reformers call for governance structures that better reflect the distribution of economic power in the twenty-first century. These debates matter.

The institutions were created at a particular moment in history. They emerged from a world in which economic power, financial capital, institutional capacity, and technical expertise appeared concentrated within the same societies. Their authority rested not simply on formal mandates or material resources, but on a broader belief that those exercising power also possessed the knowledge necessary to guide the international economy. For much of the postwar era, that alignment appeared stable because the institutions seemed capable of delivering the outcomes they promised: stability, growth, development, and economic cooperation.

The contemporary crisis emerged because that alignment has weakened. Economic power has become more geographically distributed. Alternative development experiences have produced competing interpretations of economic success. Expertise has become more decentralized, more contested, and less easily monopolized by any single institution. Yet many of the structures through which authority is exercised remain rooted in assumptions formed under very different historical conditions. The result is a widening gap between the world that produced the institutions and the world they are now asked to govern.

This helps explain why contemporary disputes extend far beyond representation. The argument no longer concerns only who governs. It concerns who possesses the authority to define necessity, stability, risk, responsibility, development, and economic success itself. At stake is not merely the distribution of power within institutions, but the relationship between power, expertise, and legitimacy that allows institutions to exercise authority in the first place.

This is also why governance reform, while important, cannot fully resolve the challenge. Voting shares can be adjusted. Board representation can be expanded. Leadership arrangements can be renegotiated. None of these changes automatically restore confidence in the assumptions through which authority is exercised. Institutions may alter their structures without resolving questions about the legitimacy of the ideas that continue to guide them.

The IMF and World Bank are not experiencing a crisis because power has changed. Institutions routinely survive shifts in power. They are experiencing a crisis because the relationship between power, expertise, and legitimacy that once sustained their authority is no longer taken for granted. The assumptions that once appeared universal appear contingent. Frameworks that once seemed self-evident appear contestable. Expertise that once commanded deference encounters scrutiny.

The question confronting the IMF and World Bank reflects a broader challenge facing contemporary institutions: how does authority remain persuasive when expertise becomes contested? That question remains unresolved. Institutions can survive policy disagreements. They can survive governance disputes. They can even survive repeated crises. What they struggle to survive is the gradual separation of power, expertise, and legitimacy that once reinforced one another. When authority is no longer accepted as the natural consequence of expertise, institutions must find new foundations upon which legitimacy can rest.

Recognition of this problem is no longer confined to critics of the Bretton Woods institutions. Speaking at the World Economic Forum in Davos in January 2026, Canadian Prime Minister Mark Carney argued that the international system was experiencing "a rupture, not a transition" and that "the old order is not coming back." His observation reflected a growing recognition that institutions created under one historical configuration of power may struggle to maintain authority when the conditions that originally sustained that authority have fundamentally changed. Similar concerns have emerged among European leaders. Speaking at Davos, German Chancellor Friedrich Merz argued that an international order based on commonly accepted rules could no longer be assumed. These observations align with a broader scholarly assessment that the Liberal International Order itself is now deeply contested. Together, they point toward the same conclusion: institutions built for one distribution of power, authority, and expertise may find it difficult to sustain legitimacy under another.

The world that created the IMF and World Bank is gone. The challenge now is whether institutions built for that world can develop a form of legitimacy capable of surviving the one that replaced it.